Because of the Ability to Override Internal Controls

B employee fraud because of the irregular hours worked by some employees. Fraud committed by a company president.

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Ability of management other personnel andor third parties to circumvent controls through collusion.

. Greater for employee fraud because of the higher crime rate among blue collar workers. Fraud committed by a company president. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud.

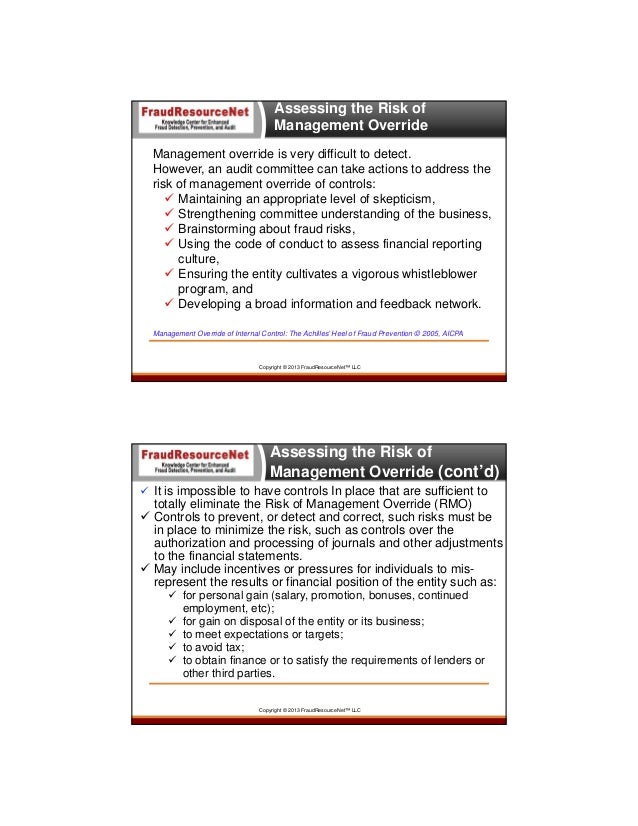

When the opportunity to override internal controls is combined with powerful incentives to meet accounting objectives senior management may engage in. Management override of controls whether the entity is publicly held private not-for-profit or governmental. Fraud Examination with ACL CD-ROM 3rd Edition Edit edition.

Fraud committed by lower-level employees is more difficult to detect because those employees more often have the ability to override internal control procedures. C greater for employee fraud because of the higher crime rate among blue collar workers. Fraud committed by a company president.

Of internal control the entity is always exposed to the danger of management override of controls whether the entity is publicly held private not-for-profit or governmental. C greater for employee fraud because of the higher crime rate among blue collar workers. Employee fraud because of the higher crime rate among blue collar workers.

Greater for management fraud because managers are. B greater for management fraud because of managements ability to override existing internal controls. 5 Internal controls are not designed to provide reasonable assurance that 5 A the companys resources are used efficiently and effectively B company personnel comply with applicable rules and regulations C transactions are executed in accordance with managements authorization.

A greater for management fraud because managers are inherently more deceptive than employees. Fraud committed by a company president. Solutions for Chapter 3 Problem 6MC.

Greater for management fraud because of managements ability to override existing internal controls. Fraud committed by a company president. That Practice Alert is included as Appendix C to this book.

Greater for employee fraud because of the. Greater for management fraud because managements ability to override existing internal controls. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud.

Greater for management fraud because managers are inherently more deceptive than employees. Fraud committed by a company president which of the following refers to the circumstances taken as a whole that would lead a reasonable prudent professional to believe fraud has occurred is occurring or will occur. And External events beyond the organizations control.

03-2 Journal Entries and Other Adjustments provides additional guidance on the procedures you should consider to review journal entries and other adjustments for signs of management override of internal control. When the opportunity to override internal control is combined with powerful incentives to meet accounting. Manipulation of stock price.

Accounting questions and answers. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud.

Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud. PITF Practice Alert No. Management fraud because of managements ability to override existing internal controls.

C management fraud because of managements ability to override existing internal controls. Override of internal controls is due to pressures or incentives to meet the business objectives or perhaps an opportunity for the management to engage in fraudulent activities and misuse their authority to cover up in the financial statements. Management fraud because managers are inherently smarter than employees.

A employee fraud because of the larger number of employees in the organization. Regarding overriding or circumventing internal controls The PCAOB states that Management is in a unique position to perpetrate fraud because of its ability to directly or indirectly manipulate accounting records and prepare fraudulent financial statements by overriding established controls that otherwise appear to be operating effectively. B greater for management fraud because of managements ability to override existing internal controls.

D all frauds will be detected. Greater for management fraud because of management s ability to override existing internal controls. Fraud committed by a company president.

This problem has been solved. The motivation for management to override internal controls could include things such as. A greater for management fraud because managers are inherently more deceptive than employees.

Greater for management fraud because managers are inherently smarter than employees. Mechanics of Overrides. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud.

Which of the following refers to the circumstances taken as a whole that would lead a reasonable prudent professional to believe fraud has occurred is occurring or will occur. Dependence on financial results for receiving bonuses or other benefits. D management fraud because managers are inherently smarter than employees.

Collusion refers to the act of two or more individual circumventing internal control procedures. Because of the ability to override internal controls it is usually most difficult to prevent which type of fraud. Need to meet debt covenants or other benchmarks imposed by lenders or investors.

Ability of management to override internal control.

Management Override Common Tactics And How To Audit For Red Flags

Asec As3300 Series Easy Code Change Digital Lock With Key Override Optional Holdback In 2021 Digital Lock Coding Digital

Auditors Responsibility For Fraud Detection

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Management Override Common Tactics And How To Audit For Red Flags

Limitations Of Internal Control Accounting Hub

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

2

Management Override Common Tactics And How To Audit For Red Flags

2

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Au 319 Consideration Of Internal Control In A Financial Statement Audit Pcaob

Download Redgate Smartassembly V7 5 0 4261 Keygen Control Flow Spaghetti Code How To Become

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Define And Explain Internal Controls And Their Purpose Within An Organization Principles Of Accounting Volume 1 Financial Accounting

Combating Fraud Through Effective Internal Controls Boardandfraud

Directorial Override Walkthrough Control Wiki Guide Ign

Limit Selector And Override Controls Basic Process Control Strategies And Control System Configurations Automation Textbook

Comments

Post a Comment